A week defined by a fragmenting Fed, record chip sector returns, and a stagflation print the market chose to ignore.

Global Macro

- Fed held the funds rate at 3.50 to 3.75 percent for the third consecutive meeting. Vote was 8-4 on the policy action, the most dissents since October 1992.

- Miran wanted a 25bp cut. Hammack, Kashkari, and Logan supported holding rates but rejected the easing bias in the statement.

- Powell's last meeting as Chair. Term ends May 15. He stays on as Governor through January 2028. Warsh nomination advanced to the full Senate.

- Markets are now pricing no further cuts through 2026, with non-zero probability of a hike in 2027.

- Q1 GDP printed +2.0 percent annualized, rebounding from +0.5 percent in Q4 2025. The Q4 number was compressed by the federal shutdown, so the rebound is partly mechanical.

- Q1 PCE price index +4.5 percent annualized, up from +2.9 percent in Q4. Core PCE +4.3 percent. This is the inflation re-acceleration the Fed is now staring at.

- March headline CPI +3.3 percent YoY, the highest since May 2024. Gasoline +21 percent YoY.

- ISM Manufacturing prices paid hit a 4-year high. Initial jobless claims fell to the lowest level in nearly 50 years.

- Iran war remains the macro anchor. Strait of Hormuz effectively closed. Crude posted a second consecutive weekly gain despite a Friday pullback.

- 10Y Treasury closed at 4.39 percent (off a 4.45 percent nine-month high midweek). 2Y at 3.88, 30Y at 4.97.

- Japan intervened in FX Thursday after USDJPY breached 160.72 (two-year high). Pair closed at 156.54 Friday.

- Pentagon signed expanded AI agreements with Nvidia, Microsoft, Reflection AI, and Amazon for use on classified networks. Spirit Airlines filed for bankruptcy.

S&P 500

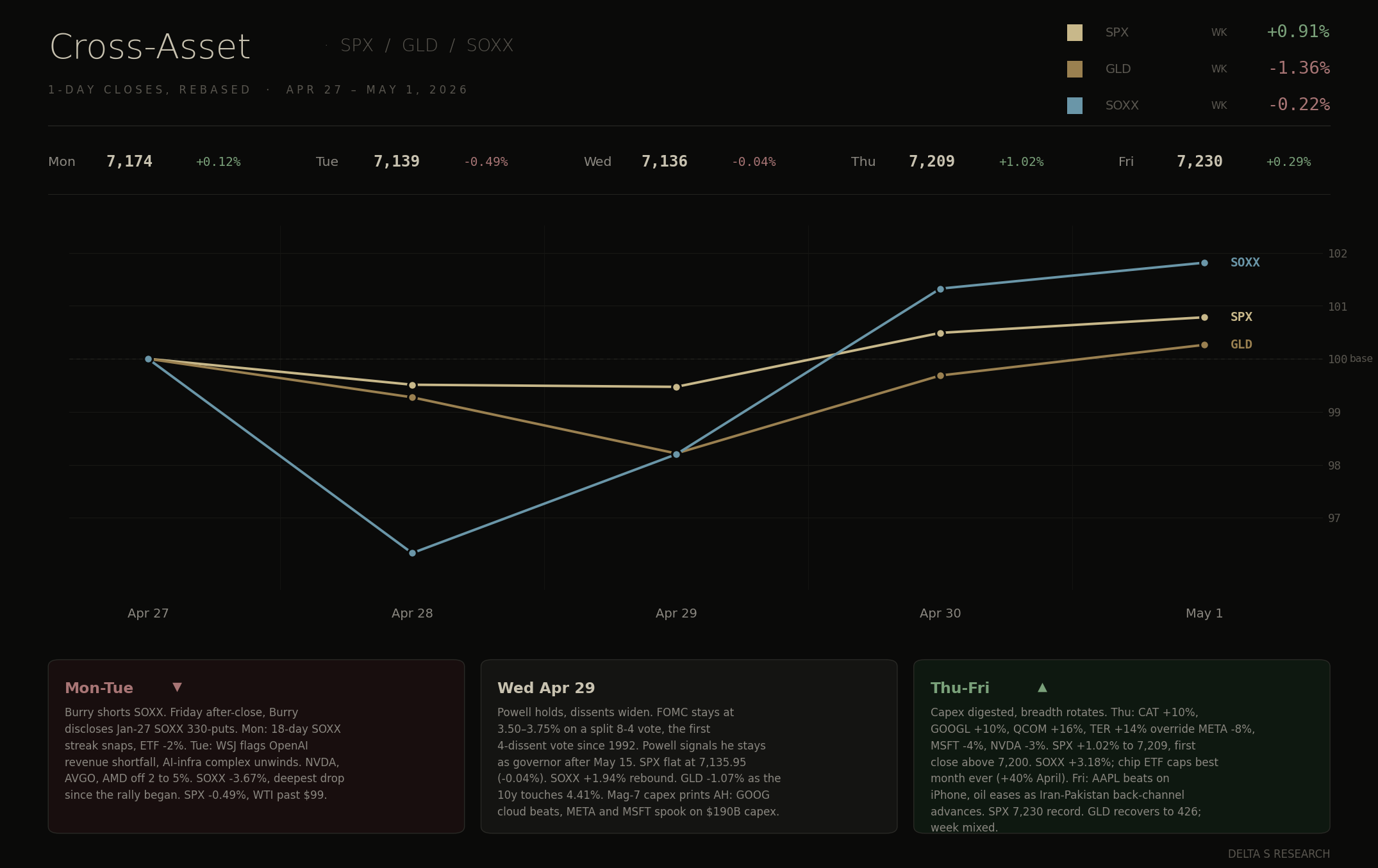

- Closed 7,230.12 on Friday. Up 0.9 percent on the week. Sixth consecutive weekly gain, the longest streak since October 2024.

- Nasdaq closed at 25,114.44, also a record.

- Q1 earnings season is exceptional. 84 percent beat rate vs 78 percent five-year average. Surprise magnitude 20.7 percent vs 7.3 percent average. EPS growth tracking the highest since Q4 2021.

- Alphabet, Amazon, and Meta delivered the biggest contributions to the upward earnings revision.

- Apple beat Friday with a constructive forward guide despite an iPhone revenue miss. Stock +3 percent.

- Caterpillar beat with record backlog citing AI data center power generation demand.

- Exxon and Chevron beat but profits fell as oil compressed downstream margins.

- Roblox cut full year guidance and traded down 24 percent premarket Friday.

- Forward 12-month P/E now 20.9 vs 5-year average 19.9 and 10-year 18.9. Multiple expansion is doing more work than earnings.

- VIX closed near 17. Risk premium remains compressed.

Semiconductors

- Best month on record for the chip sector. SOXX +40.4 percent in April, the largest monthly return in the fund's 25-year history. SMH +32.2 percent, also a record.

- SOX printed 17 consecutive green sessions, surpassing the prior record of 15 set in 2014.

- SOX week +3.71 percent, month +33 percent, year-on-year +144 percent.

- Leadership inverted. Nvidia +21.9 percent in April, strong absolute, weak relative.

- AMD +75 percent. Marvell +64 percent. Astera Labs +84 percent. Credo +88 percent.

- The market is repricing the second tier of chip designers and AI infrastructure names that NVDA's premium had ignored through 2024 and 2025.

- Friday: NVDA underperformed after WSJ reported OpenAI missed internal revenue and growth estimates.

- NVDA reports earnings May 20. That print is the next test for the entire complex.

Gold

- Spot gold closed near $4,630 Friday. Second consecutive weekly decline.

- Down approximately 15 percent from the all-time high of $5,595.42 set on January 29.

- The selloff is mechanical. Energy-driven inflation forced markets to price out Fed cuts and price in a 2027 hike. Real yields backed up. Higher-for-longer compresses gold's opportunity cost case.

- WGC reported central bank reserve accumulation continued in Q1. Marginal flow has not been enough to offset the rates repricing.

- Thursday's nearly 2 percent rebound came on dollar weakness following the Japan FX intervention, not gold-specific buying.

- Structural bid from de-dollarization remains intact. The cyclical headwind from rates is the active driver.

Trades This Week

- NVDA bull put spread closed Monday. Premium harvested. Thesis: NVDA has a strong magnet around the $190 strike and the position decayed cleanly into expiration.

- LITE (Lumentum) bull put spread opened, expiring May 8. Earnings May 5 after close. Trade is harvesting the elevated IV crush around the print while remaining structurally bullish on momentum.

- Lumentum is one of the cleanest pure-play exposures to the optical supercycle. The 800G to 1.6T transceiver transition is the bottleneck for AI cluster scale-up, and LITE's 200G-per-lane EML laser is currently the only technology supporting 1.6T at scale.

- LITE was added to the S&P 500 in March. Stock has gone from roughly $150 in early 2025 to north of $800 in April 2026.

- Hyperscaler capex and the OCS roadmap remain tailwinds. Execution risk on capacity scaling is the main bear case.

- MU (Micron) bull put spread sold, expiring May 8. Bullish. Memory super-cycle, HBM demand, and DRAM pricing tightness all confirmed by SanDisk's Thursday print.

- CIFR (Cipher Mining) diagonal call spread opened. Long-term bullish thesis: BTC mining recovery plus the AI and HPC data center pivot.

- SNDK position closed. Opened last week ahead of the April 30 print. The earnings were a blowout:

- Q3 revenue $5.95B vs guide $4.4B-$4.8B. Up 97 percent sequentially, 251 percent YoY.

- Non-GAAP EPS $23.41 vs estimate $14.36. Beat by 63 percent.

- Non-GAAP gross margin 78.4 percent vs guide 65 to 67 percent.

- Datacenter revenue +233 percent sequentially, +645 percent YoY.

- Q4 guide: revenue $7.75B-$8.25B, EPS $30-$33.

- Zero long-term debt. $6B share buyback authorized.

- Calendar 2026 datacenter growth outlook revised to mid-70s percent from 60s.

- Gold position closed. Cyclical rates headwind dominates the structural bid.

Looking Ahead

- May 6: ADP. May 8: NFP, unemployment rate, Michigan inflation expectations. May 12: April CPI.

- A hot CPI print plus the Fed's fragmented stance is the asymmetric risk for next week.